Conventional Mortgage: This is where you have 20% or more of the purchase price to put down by the time you take possession (the down payment). This is the easiest loan to qualify for and is usually paid back over 25 or 30 years. The more years, the lower the monthly payments. This type of mortgage is the best deal for buyers. It is often easier to qualify for these mortgages at credit unions than at banks. (See section on Mortgage Stress Test)

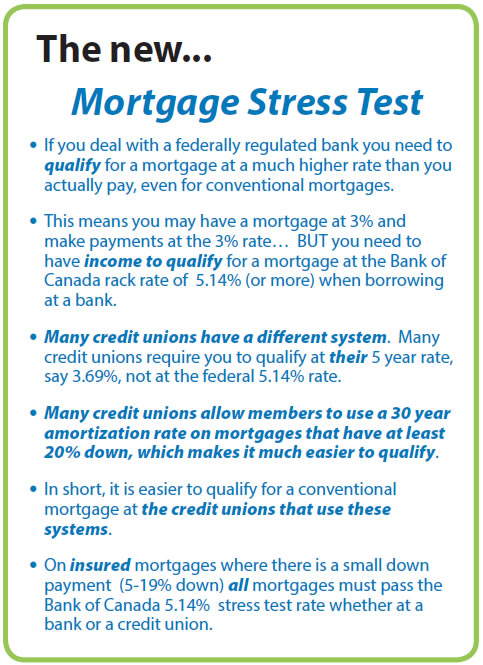

Insured Mortgage is when the down payment is less than 20% of the purchase price. The minimum down payment is 5% of the purchase price. Any down-payment less than 20% requires an insured mortgage. When you move into your new home a government insurance fee is blended into your mortgage. This fee goes to a federal government agency called the Canada Mortgage and Housing Corporation (CMHC) that will repay your mortgage to the lender if you default. This insurance adds 4% to your costs for a 5% down mortgage, or 2.8% to your costs if you have 15% down. These mortgages are written for 25 years and your income must qualify at the Bank of Canada rack rate, currently 5.14%, even if the rate you are actually paying is under 3%. With an insured mortgage you will be treated the same by a bank or a credit union. (See section on Mortgage Stress Test)

Non-Resident Mortgage: This is where the buyer is not a Canadian nor a landed immigrant. In this case the buyer will need at least 40% down and will face other hurdles.

Other things you should consider about mortgages:

You need to show income to qualify for a mortgage. Several factors can affect how much you can borrow. If you are not getting good results, consider a different lender or mortgage broker.

For a very rough estimate of how big a mortgage you can qualify for, take your total household annual income before deductions and multiply by 4.5 for a credit union mortgage, or multiply by 4 for a bank mortgage. For example if you and your spouse/partner have a gross annual income of $100,000, you may qualify for a $450,000 mortgage. Other credit factors can affect these numbers either way.

The buyer usually has the option to fix the interest rate for a certain number of years. The longer you fix it for (the term of the mortgage), then usually the higher the interest rate. If you want the lowest rate and are willing to take a risk, then go with a short term. Possible long term savings are possible by opting for variable rate mortgage with the rate you pay going up and down with the market interest rates.

If you have trouble qualifying for a mortgage, some people ask a relative or close friend to co-sign the mortgage, which means they agree to pay if you don’t.

When talking to your bank or credit union use the price including the GST so that the GST cost is included in your mortgage.

Be careful! Many mortgage companies want you to buy life insurance for your mortgage, this is optional. Often mortgage companies charge double the price for life insurance compared to what you can get on a term life insurance policy from a life insurance company.

Other things you should consider about mortgages:

Other things you should consider about mortgages: